A coalition in Kansas has come together to push reform of the payday loan industry.

Kansas For Payday Loan Reform is calling on legislators to tighten state regulations, saying the lenders are profiting from people in need.

“Across the state, people get into an emergency situation trying to cover a basic need and when traditional options aren’t available, folks turn to short-term loans,” said Shanae’ Calhoun, executive director of Topeka JUMP, heading up the coalition. “What they think is a solution ends up being a trap that is hard to get out of.”

The group supported a bill in 2021 before the House Committee on Financial Institutions and Rural Development. The coalition worked to educate the legislators on HB2189, but there was no formal hearing, and it was never brought to a vote. In 2022, it was reintroduced, and again, never made it to the floor.

The committee’s ranking minority party member, Rui Xu, said committee leadership and others discussed the bill informally and there was interest from both sides of the political aisles, “but then nothing ever happened,” he said.

Republican Jim Kelly, chair of the Financial Institutions committee, said he was trying to put together a process where the consumer reform group and lenders could come together and craft a bill to put in front of the House for a vote.

“The ideal, for me, is to have a compromise brought to us and then see how it starts moving along,” Kelly said. “I think you end up with a lot more unintended consequences if the legislature itself tries to draft it or if one party has it and they aren’t open to looking at any other options.”

Kelly said there have been a number of similar reform bills pop up, but this was the most progress he’s seen made during his 12-year tenure on the committee.

“This is the farthest it has ever moved – that the groups got together and tried to work something out,” he said. “The consumer group was better organized this year than ever before, so that helped move it forward.”

Andy Sanchez, executive secretary-treasurer for the Kansas State AFL-CIO, which is part of the coalition, said the payday loan industry is one of the many powerful lobbies in Kansas. Passing any kind of regulation won’t be simple.

“I think certain issues rise to the top during a typical legislative session and this, we hope, is going to be one of them,” he said. “We have to make sure this stays in the public eye.”

Small Money Lending 101

Payday loans are short-term, unsecured loans. They are typically used by people who can’t get money from banks. They often only require the borrower to be 18 or older, have a job and have a driver’s license.

The amount eligible for lending is based on state regulations and is set at $500 or less in Kansas and Missouri. The loans usually need to be paid back in a lump sum in two weeks to a month. They are for short terms, in low amounts, are available immediately and are simple to get. But interest rates are typically very high – with an annual percentage rate (APR) of up to 391% in Kansas and 371% in Missouri.

Despite such high interest rates, many people seek financing from the payday loan industry. The Pew Charitable Trusts, which focuses on payday lending as part of its consumer finance focus, estimates about 12 million Americans use payday loans annually. Worldwide, the industry was worth about $33.5 billion in 2021 and is expected to grow to more than $42 billion by 2028, according to the Vantage market research organization.

“This is a fairly straightforward product and consumers understand their financial situation and, for some, this may be the best option for them at any particular point in time,” said Ed D’Alessio, executive director of INFiN, a trade association that represents consumer financial products including small-dollar lenders.

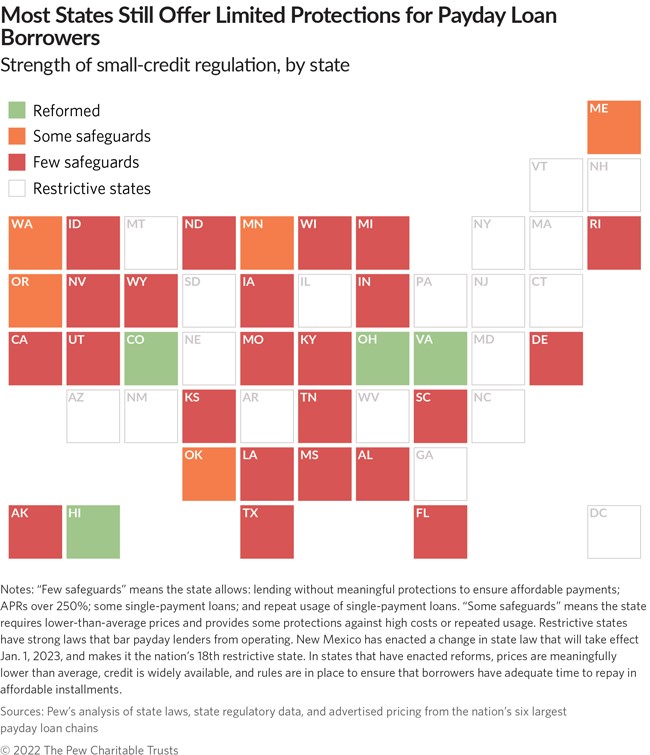

But groups like the coalition in Kansas have been pushing back on the industry in recent years. Payday lending is not permissible in more than a dozen states. In a handful of others – including Ohio, Hawaii, Montana and Colorado – legislation has been passed that effectively puts the lenders out of business. This legislation, along with the proposed legislation in Kansas, takes aim at a few key lending regulations.

The first is APR. If a person takes out a $500 loan in Kansas, he would pay about $161 in interest over a month’s time. HB2189 would cap the APR at 36%, a number chosen for many states’ reform. That would make the interest on that same loan about $15.

But D’Alessio said that rate effectively forces these lenders out of a state.

“It really equates to a number that makes the product not viable,” he said. “It allows a lender to charge $1.38 for a $100 two-week loan. Therefore, where we see 36% caps imposed, they are not banning it, but no one can provide that product. Lenders have to have an appropriate return to keep their doors open.”

The second point HB2189 takes on is payback. Borrowers are currently required to pay back loans in a lump sum at the due date. The proposed legislation allows borrowers to pay back their loans in equal installments over time including the principal, interest and fees.

This is important because someone short on cash often can’t pay back the principal and the interest in one chunk.

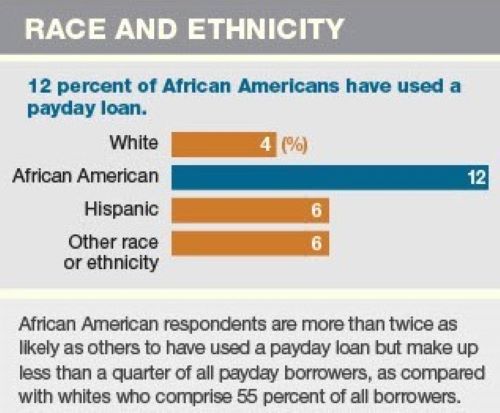

According to Pew, the average payday loan size is $375, for which borrowers end up paying $520 in interest. Average small-money borrowers take out eight loans in one year, for about 18 days each, meaning people carry such debt for almost five months a year. Three-quarters of these loans are taken out within two weeks of the original, meaning the borrowers don’t have enough money to pay back the loan and make it to the next payday.

According to a study by the Federal Reserve Bank of Kansas City, payday lenders depend on repeat borrowing to make profits. The high margins on repeat loans offset the high cost of default rates – which can be upwards of 20% — and managing new customers.

“Converting occasional payday borrowers into ‘chronic’ borrowers is an important source of profits for payday lenders,” the report noted.

The legislation in Kansas would help curb this by prohibiting lenders from having more than one outstanding loan per borrower at a time.

“Institutions like payday loan lenders have become exploitative of people who live paycheck to paycheck,” Sanchez said.

D’Alessio makes a couple of arguments for preserving payday loans.

First, he noted that these bills go after small-dollar lenders working under state regulations. The concern, he said, should focus on the vast number of providers on the Internet who aren’t regulated by state or federal laws. These lenders charge even higher interest and fees and can pursue collections forcefully. When states aim reform at regulated products, it leaves the market ripe for online lenders. According to Pew data, about one-quarter of people get payday loans online, instead of at storefront, institutions.

“If there are bad actors out there, go after them, we support that,” D’Allessio said. “That doesn’t help anybody.”

Secondly, the laws that permit and regulate these products weren’t created by the industry, but by states.

“They (legislators) had the opportunity to study the products, study the cost, and they felt that this was an appropriate amount for a lending charge,” he said. “Small-dollar loans only exist by the virtue of statutory enactment … legislators saw an understanding of the need for these loans for people who don’t have access to bank products.”

Faith in the Process

The coalition is hoping to persuade those legislators to reform the industry.

Topeka JUMP began hearing about payday loan debt from its constituents at its inception seven years ago. But they were a nascent organization that worked on issues at the city level. This was going to be fought at the state level.

So, in 2019, they created this coalition that now has about 30 organizations including Habitat for Humanity, March of Dimes and United Way. But its major strength, she said, is its faith-based backing.

“A lot of denominations that don’t have much room to work on anything else together are here,” she said.

Social justice groups from Catholic, Methodist and Episcopalian organizations in Kansas are all taking part in the effort.

Reverend Sarah Marsh, mercy and justice coordinator for the Great Plains Conference of the United Methodist Church, said it has been easy for different faiths to get behind payday loan reform.

“It’s a moral issue that isn’t hard to understand when you have just a few facts in hand,” she said. “United Methodists are a diverse bunch of people, but this is an issue we can all get behind and wholeheartedly join.”

Marsh is responsible for helping congregations build the capacity to work on important issues. But for her, this was the first time to take on a larger campaign.

“We are learning to work in a coalition, which is so valuable,” she said. “And once we’ve built these networks and relationships they aren’t going away. We will be ready to work together when the next issue comes up.”

Rabbi Moti Reiber, executive director at Kansas Interfaith Action, a multi-faith advocacy organization, said colleagues in other states, including Ohio, have worked on payday loan reform, so he knew it could be successful.

In Ohio, the APR on small-money loans is 124% and borrowers can pay the funds back in installments (only a handful of states have rates below 200%), according to data by Pew. This rate would make a $500 loan cost about $51 over 30 days.

Though HB2189 calls for a 36% interest rate cap, Reiber said the group isn’t tied to that number, but wants to get all parties at the table to negotiate a reasonable bill.

“Last year, we showed a willingness to come up with something the industry could work with, but the conversation never came to fruition,” he said. “The only reason they have to work with us is if the legislators tell them they need to do it. And we haven’t gotten to that point yet.”

To make the issue a priority, it needs to get above the din. And Reiber said the Catholic church, with their expansive reach statewide, has been crucial in doing that.

“It’s an injustice that people in desperate situations are being taken advantage of,” said Deacon Bill Scholl, consultant for social justice for the Catholic Archdiocese of Kansas City in Kansas. “We feel called to be good citizens by contributing to policies that are good for everybody; that provide conditions in which everybody in the community can thrive.”

The Kansas Catholic Conference lobbies politicians and educates congregants to get engaged in a range of issues including pro-life, immigration, access to medical care and just wages, Scholl said. He echoes the desire to work on ways to set limits that serve the common good while enabling businesses to operate.

The coalition plans to put a bill in front of legislators during the upcoming session. Until then, they will hold rallies and get the word out through social media and letters to the editor of Kansas media outlets. Calhoun said they will do the most they can with their people power and shoestring budget.

“The industry has a well-organized, well-financed campaign to maintain the status quo,” Scholl said. “And legislators, to push against the grain, need support from other representatives and from constituents who will say, ‘Hey, we have your back and will remember that you did what was right when it’s time to vote next.”

Tammy Worth is a freelance journalist based in Blue Springs, Missouri.

Reading these stories is free, but telling them is not. Start your monthly gift now to support Flatland’s community-focused reporting.

Related Stories

KCK steps up work on school buildings promised with $180 million bond package

The Kansas City, Kansas, school district provides an update on several school construction projects.

Nick’s Picks | Ballots, Bribery, Baby and More …

The World Cup has left town, some some of the biggest headlines are a man stuck in the toilet of a Porta Potty, upcoming elections, and an alleged scandal in Jackson County.

Nick’s Picks | Fireworks, Heat, Dylan and More …

As America gets set to celebrate the 250th anniversary of the Declaration of Independence, the fireworks are not the only things that will be hot. Expect heat and humidity this week.