Borrowers Weigh Options as Student Loan Payments Resume Nearly 45 Million Americans Collectively Owe More Than $1.7 Trillion

Published November 1st, 2023 at 12:48 PM

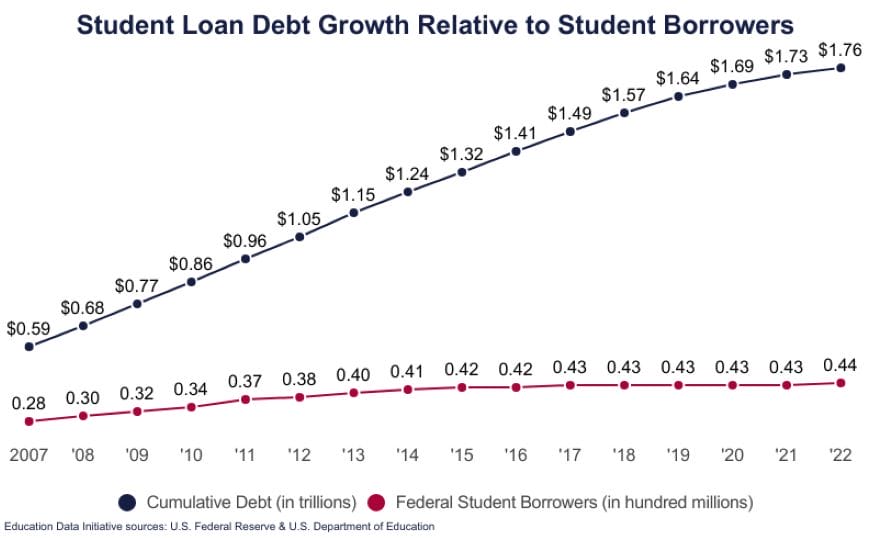

Above image credit: Nearly 45 million Americans collectively owe more than $1.7 trillion in 2023 and have an average outstanding loan balance of less than $25,000, according to a Federal Reserve report in 2022. (Getty Images)Justin Brown, a father of a 2-year-old who lives with his wife in the St. Louis area, has $20,000 in student loan debt.

Before the pause on loan payments at the start of the COVID-19 pandemic in 2020, he paid $300 a month. But now that Brown has a family, his financial responsibilities have grown — paying for child care, a mortgage for a house he bought in 2022 and car notes, to name a few.

“I have to look at that $300, like where do I carve it from? Because my income is not going to increase in the next month, and maybe in the near future, but here and now it is what it is and my wife’s is what it is,” said Brown, who works in marketing.

“I have to now make a sacrifice and the sacrifice is not going to come at the expense of my kid and it’s not going to come at the expense of my marriage. But it will come at the expense of something that I can live without that I otherwise would choose to (spend money on). It may mean I may eat out two times a month instead of 10 times a month or that I won’t go to the movies ever again.”

Many borrowers, like Brown, are facing similar decisions this month as student loan payments resumed. Nearly 45 million Americans collectively owe more than $1.7 trillion in 2023 and have an average outstanding loan balance of less than $25,000, according to a Federal Reserve report in 2022. They pay an average between $200 and $299 monthly, according to the Fed.

Economists say that hundreds of dollars spent on monthly student loan payments is a loss to the economy and could hurt consumer spending, affect workers’ decisions to stay at their current job or look elsewhere, and delay new home purchases or renting a nicer apartment.

According to a CNBC online poll in January 2022 of 5,162 adults, 81% of borrowers surveyed said they delayed major decisions because of their debt, with 33% deferring a home purchase, 35% setting aside travel plans, and 12% waiting to look for a new job.

“It will be a decline in demand, a decline in overall spending in the economy,” said Mike Konczal, director of macroeconomic analysis at the Roosevelt Institute. “A year ago, people were very worried that there was too much spending in the economy. Now, there’s a little less worry about that and a lot more worry about the real uncertainty that’s going to happen over the next year.”

Konczal said that he sees the resumption of student loan payments as the biggest headwind the economy is facing right now. Less spending in the economy has historically helped trigger a recession, he said. Consumer spending represents two-thirds of economic activity.

Higher education has been associated with higher home ownership rates, but having student debt is associated with lower rates of owning a home, according to findings from a 2017 New York Fed report.

Early in the pandemic with interest rates low and the pause on loan repayments, younger buyers took advantage of the market to buy homes. And while student debt isn’t the biggest roadblock today to home ownership (high mortgage rates are), such purchases will be impacted as potential buyers are faced with student loan repayments, instead of putting that money toward a down payment, according to Selm Hepp, chief economist for CoreLogic.

“If you’re saving that much on a monthly basis over a year, how much of that could help you with the down payment,” Hepp said.

The same holds true for those seeking to upgrade their rentals.

“While we expect to see rent growth go back to the rate that was pre-pandemic, which is like 3% to 4% on a year-over-year basis, which is what we’ve historically seen, that may be subdued because of the student loan payments. So people may not be able to upgrade to that nicer apartment but they’ll just kind of stick it out wherever they are because they now have that student loan (payment),” Hepp said.

Major retailers have already expressed concern over the impact of student loan payments on their businesses. Executives from Macy’s, Walmart, and Target said in August that they were keeping it in mind as a source of financial pressure on consumers.

The Biden administration’s plans last year to cancel up to $20,000 of student loan debt would have helped many borrowers, particularly Black and Latino borrowers. But the U.S. Supreme Court struck down the policy in June. Then in August, the administration announced steps to reduce the financial burden of making payments for some borrowers by basing them on their income and family size and not borrowers’ loan balance.

The Federal Reserve also has recognized the return of student loan payments as it considers future policy. On Sept. 20, Fed Chair Jerome Powell was asked what he thought the looming government shutdown, rising oil prices, and the UAW strike meant for the course of Fed policy.

Describing a “collection of risks,” Powell said, “There is a long list and you hit some of them. It’s the strike, it’s the government shutdown, resumption of student loan payments, higher long-term rates, oil price shock. There are a lot of things that you can look at, so what we try to do is assess all of them and handicap all of them. Ultimately though, there’s so much uncertainty around these things.”

Labor Market

Economists point out that research has shown that student debt and debt cancellation affect borrowers’ decisions about the jobs they take or don’t take. When people have their loans discharged, they are more likely to move, which researchers say suggests they are able to pursue opportunities they wouldn’t otherwise have with the student debt. Some research has also shown that debt motivates graduates to favor higher-paying jobs over lower-paid jobs that are more focused on the public interest.

“There is evidence that holding student debt affects people’s choices early in their careers. I found that it affected people’s occupational choices,” said Jesse Rothstein, professor of public policy and economics at the University of California, Berkeley, and co-author of the research on job choices.

Because a college degree doesn’t bring the same accumulation of wealth that it once offered, economists are also concerned that there is little payoff for households constrained by payments.

A St. Louis Fed report released in 2019 found a decline in the wealth a college degree brings over the past few decades. Families whose head of the household was born in the 1980s have a weaker college wealth premium, “to the point of statistical insignificance.” The exception is white families where the head of the household has a bachelor’s degree, but even then the wealth enjoyed by those families is much smaller than in older groups.

Lissa Knudsen, a PhD candidate at the University of New Mexico, who is studying health communication, has an 18-year-old who will head to college in a year herself. Knudsen has three streams of income as a freelance journalist, cheesemonger, and a teacher that have helped support her as she makes her way through school, which she said is not really enough for her to live on. She has $230,000 in student loan debt.

Unlike some borrowers, who look for well-paying jobs after graduation, she said that she is worried that if she takes a more lucrative job in her field of study, student debt will swallow up her income anyway.

“I’m afraid that there’s a disincentive for me to try to use my PhD to its fullest potential and to make say $70,000 or $80,000 a year because I think almost all of that would go to student loan payments,” she said. “Versus, if I stay in the lower income bracket, I might be able to have the minimum amount of payment. Then I could hopefully get some of it forgiven in a while. That would be great.”

Policy Implications

Bilal Baydoun, director of policy and research at the Groundwork Collaborative, observed that the return of student loan payments will undo some of the positive changes the recovery brought to households that previously felt greater financial precarity. For example, the rise of younger people, many of them millennials, buying homes earlier in the pandemic when interest rates were low and student debt payments were on pause, was a sign of a changing economic tide.

“My fear overall is that the sort of muscle memory of our pre-pandemic plutocracy is starting to redevelop … (Policymakers) want to grow different muscles. We want to grow the muscles that we’ve seen over the last couple of years of major public investment, of labor activity, of rising wages that outpace inflation and this really threatens all of that,” he said.

To address the burden of student debt on the U.S. economy, experts and economists say that the federal government needs to undertake major policy efforts on debt cancellation and overhauling the way higher education is financed.

Baydoun said that debt cancellation, once a fringe policy idea years ago, is “considered one of the most important interventions when it comes to our affordability crisis.”

“I think continuing to find ways to (cancel student debt) is not only great economic policy, it’s also great politics. All of these borrowers through the course of the pandemic, when payments were on hold for three years, they saw very clearly that nothing bad happened as a result of that … In fact, if anything, it was one of the factors that helped supercharge our economic recovery,” he said.

Not all borrowers plan to resume payments on their student loans. Kyle Guzik, a high school art teacher who lives in Richmond, Virginia, has more than $200,000 in student loan debt, most of it from William & Mary, which he attended for graduate school. He spends $1,350 in rent each month and has more than $10,000 in medical debt, which he also can’t pay. He said his daily life expenses take up the rest of his budget and that there simply isn’t anything left over.

“The money just disappears. It might seem like a lot at first but it just disappears and (student loan servicers) want whatever the amount is that they want. Alright. It isn’t there to be had,” he said. “ … You can’t get blood from a stone.”

Guzik said his decision is one of financial necessity. But he added that he hopes this refusal will result in policy changes.

“I hope that others in my situation will also think about what is really in their own rational self interest and that, by organizing a debt strike, we will collectively force a change in policy so that housing, health care, education, and a dignified retirement are recognized politically in this country as human rights,” he said.

Rothstein said he believes the pressure for policymakers to address student debt is building but that most of it has been around canceling payments rather than redesigning the college finance system.

“We are going to need to redesign the way we pay for college and that will be a major lift before we get to the point where Congress passes something,’’ he said. “ … In the long run, our failure to do that is going to be a drag on educational attainments in this country and on economic growth.”

Disclosure: Lissa Knudsen has freelanced for Source New Mexico, an affiliate of States Newsroom.

This story first appeared on the Missouri Independent, part of States Newsroom, a network of news bureaus supported by grants and a coalition of donors as a 501c(3) public charity.

It’s crucial to find a balance between helping those with student debt and maintaining fiscal responsibility. Let’s hope the plan achieves that balance.